A plain-English look at how crypto and everyday spending actually connect

Start with a coffee

You’re standing at a café. You tap your card. A second later, it beeps, and the coffee is yours. Behind that one-second tap, a surprising amount of work just happened — especially if the money behind that card lives in crypto.

Most people never think about it, and that’s the point: when it’s built well, none of the complexity shows. This is a peek behind the counter at what it takes to make that tap “just work.”

Picture two different countries

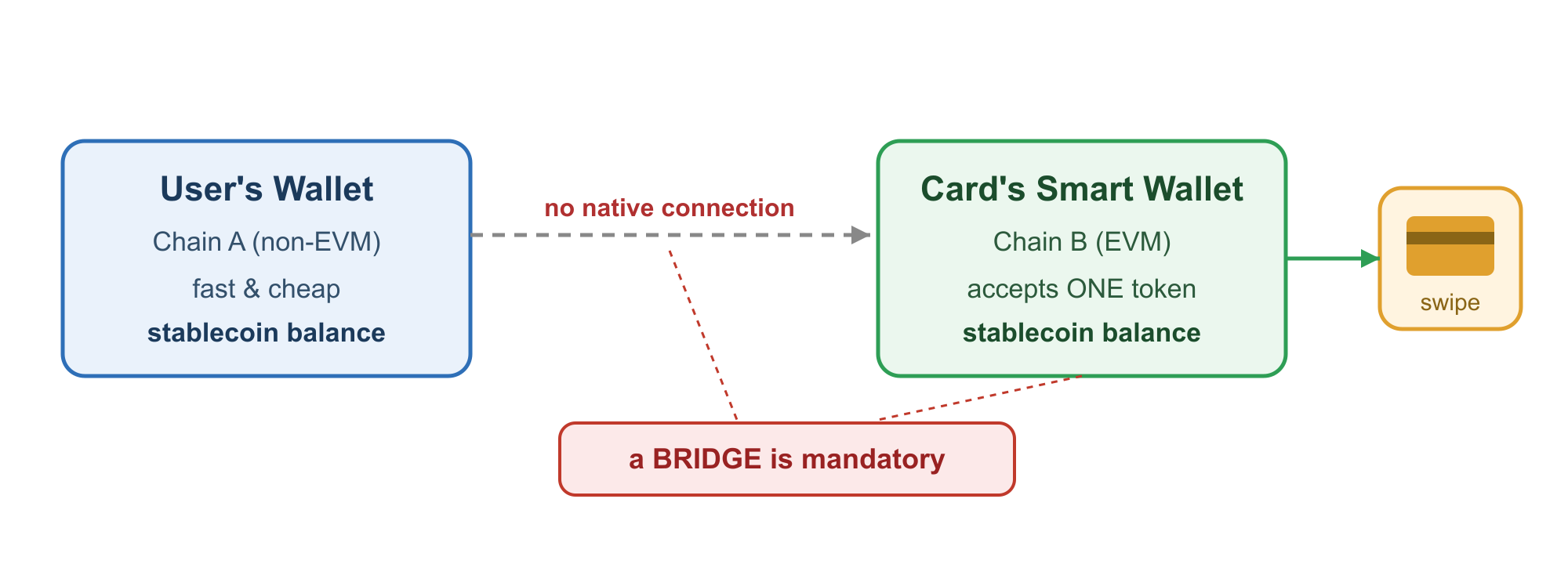

Imagine your savings are in a bank in Country A. It’s fast, cheap, and convenient. But your debit card was issued by a bank in Country B — a completely different country, with a different currency and different rules.

You want to buy a coffee with that card. Simple, right? Except the money is sitting in the wrong country. Before you can spend it, it has to actually travel from Country A to Country B and arrive in the right currency.

In the crypto world, those two “countries” are two separate blockchains that were never designed to talk to each other. They don’t share a language, a currency, or a connection. So moving money between them needs a bridge — a service that carries the money across and converts it into the exact form the card can use.

“Why not just skip the bridge?”

That’s the first thing everyone asks. So I asked the companies involved directly — the card company and the wallet company — whether the card could simply accept the money from Country A as-is.

The answer from both was a clear no. The card only accepts one specific currency, in one specific place. And getting the wallet company to support the other side would be a big project on their end, not a quick switch I could flip.

A bridge isn’t a button — it’s a small machine

“Move the money over” sounds like one step. In reality it’s several, and each one can go wrong:

- It has to deliver the exact right currency. Send the wrong version and the money technically “arrives” but can’t be spent — like wiring someone dollars when their bank only takes euros.

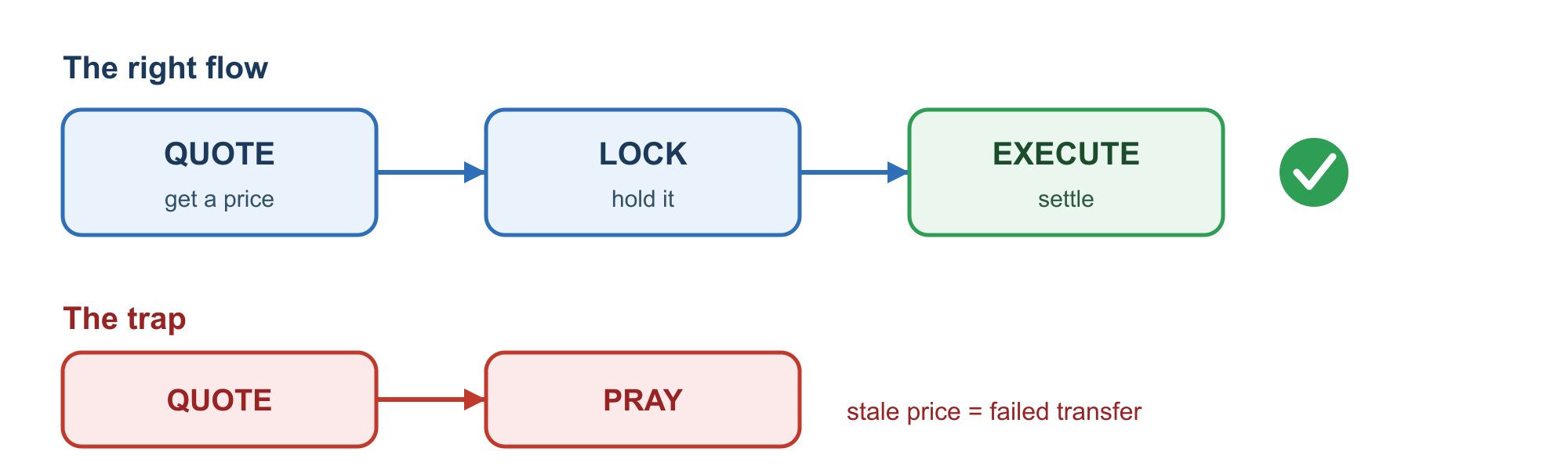

Prices don’t sit still. Exchange rates and fees shift second to second. So the system gives you a price, locks it in, and then completes the transfer — instead of quoting a number and hoping it’s still true when you confirm.

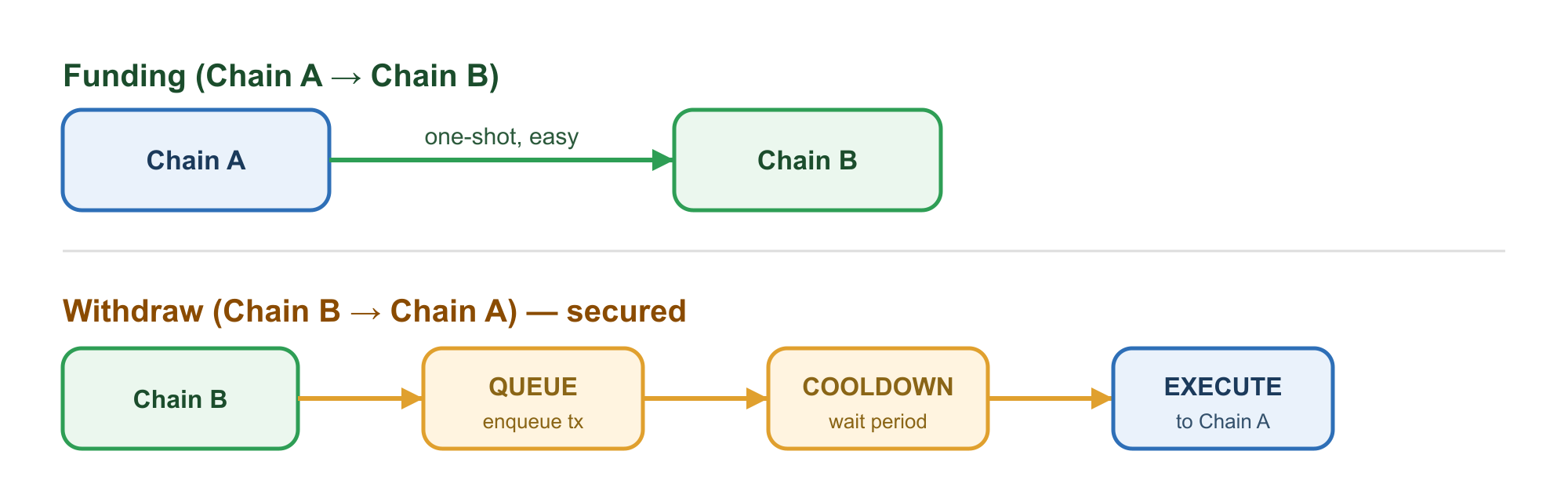

Going back out is harder than going in. Putting money onto the card is quick. Taking it back off goes through a built-in waiting period — a safety feature, like a bank holding a large transfer for review.

You always need to know where the money is. Transfers aren’t instant, so at every moment the system can answer the one question that matters: “Where’s my money right now?”

What actually happens when you load $100

- You tap “Add $100.”

- The system shows you a price (after small fees).

- You confirm, and that price is locked in.

- The money makes the trip across.

- It arrives, converted into the right currency.

- Your card balance updates — ready for that coffee.

Six tidy steps when everything works. The real skill is making it just as smooth when something doesn’t — a price that shifts, a slow transfer, a hiccup along the way.

What can go wrong (and why planning for it matters)

Most of the value isn’t in the happy path — it’s in handling the bad days gracefully. A few real examples:

- The price moves mid-transfer. If the system didn’t lock the price, you could be charged more than you agreed to. Locking it protects the customer.

- The transfer stalls. Networks get congested. A good system keeps the customer informed (“still on its way”) instead of leaving them staring at a blank screen wondering if their money vanished.

- Something fails halfway. The system has to either finish the job or safely return the money — never leave it stuck in limbo.

- A customer asks for a refund or withdrawal. Because money out takes longer than money in, the experience has to set the right expectation up front, not surprise them.

Building for these moments is the difference between a product people trust with their money and one they don’t.

The hidden part: being fair and clear about exchange rates

When you spend in your local currency but your balance is held in crypto, there’s a quiet currency conversion happening — and there are rules about doing that fairly.

The right way is to calculate the fee yourself, compare it to the official daily exchange rate that central banks publish, and show the customer plainly: “You spent €4.20; here’s exactly what that cost and the small mark-up.” No hidden surprises.

Why this matters for your business

If you’re building a product that touches both crypto and everyday money, the bridge layer is easy to underestimate. Here’s why it deserves real attention:

- Trust is the product. People forgive a slow app. They don’t forgive money that disappears or fees they didn’t expect.

- The constraints are set by your partners. What the card and wallet companies support decides what’s even possible. Confirm it early, in writing.

- Compliance is cheaper when it’s designed in. Retrofitting transparency and record-keeping later costs far more than building it from the start.

- Smooth is invisible — and that’s the goal. The better the plumbing, the less anyone thinks about it.

Plain-English glossary

Connecting two systems that were never meant to work together is, underneath, the same as any careful money handling: respect the rules, plan for things going wrong, and always be honest with people about their money. Do that well, and tapping a card for coffee “just works” — even though, behind the scenes, the money quietly crossed two entirely separate financial worlds to get there.